Digital Payments for a Futuristic World

Vpayments offers cashless payment solutions to every merchant, industry and online store, in partnership with the market leading payment provider, Worldline.

Business Payments Made Simple

In today’s competitive and dynamic business landscape you need financial solutions that are flexible and practical.

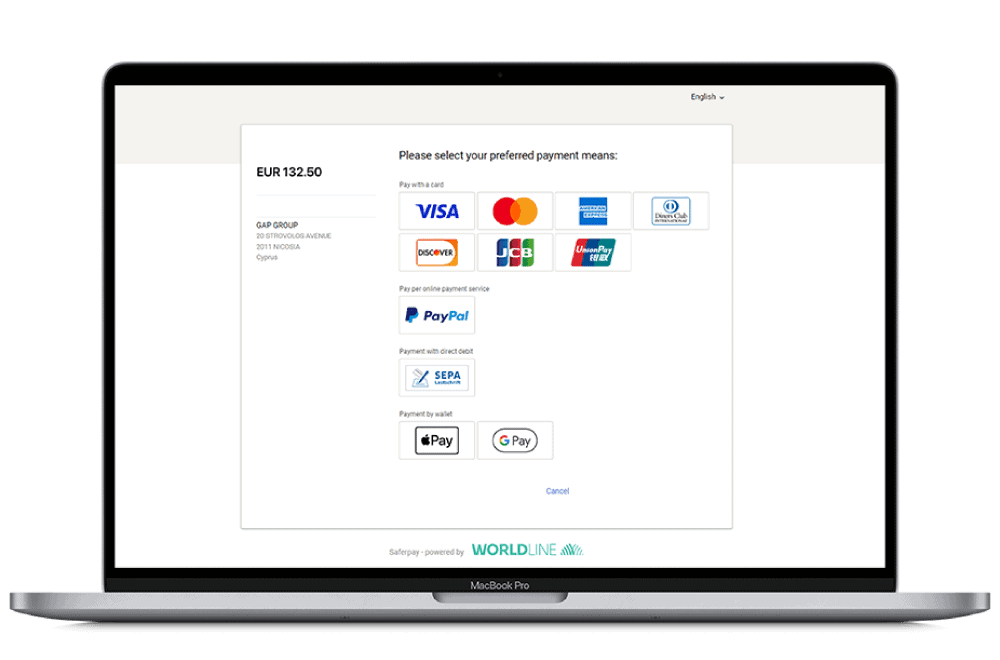

More Payment Methods More Turnover

Products for modern businesses

In today’s competitive and dynamic business landscape you need financial solutions that are flexible, versatile and practical.

Our product lineup covers terminals, card acceptance, mobile and online payments, creating a comprehensive, end-to-end financial ecosystem your business can thrive in.

Industries

The one-size-fits-all approach is a lazy, uneducated approach to financial solutions. It’s like trying to fit a square into a circle, not understanding the intricacies and minutia associated with each sector.

Our team has taken the time to research, build, test and release industry-specific solutions that are tailored to the complexity, challenges and nuances of each sector.

A few things about us

G.A.P. Vassilopoulos Group is a partner of Worldline in offering terminal infrastructure and financial acquiring services to merchants in Cyprus and across the European Union.

Latest News

Let's have a chat!

Powered by

Member of